An informed view of the challenges, opportunities and emerging trends

With the idea of blockchain as a disruptive technology gaining ground, each country is looking to chart its own path—based on both global learning and domestic ground reality. India is no exception.

India has a number of unique factors that will influence—they are already doing—how blockchain gets deployed. Broadly, they can be divided into three buckets:

Macro-economic factors

There are various macro-economic factors that potentially influence how a new high impact technology—that too something as disruptive as blockchain—gets deployed in an economy.

In case of India, the first and foremost factor that pulls everyone here is the sheer size of the market. Even in times when ease of doing business was tough, this factor alone attracted scores of business to India.

Secondly, India still stands as a hope in the not-so-exciting global economic environment, with growth predicted to be close to 88% in the next couple of years. This may impact certain technologies in both positive ways—as there will be a lot of new ideas and new investment—and negative ways—since in a high-growth environment, thrust on efficiency takes a backseat. However, India n businesses have learnt from their past experience and everybody is now looking for a profitable and sustainable growth.

Another extremely important reason, as pointed out by Jesse Chenard, co-founder and CEO of MonetaGo, the fintech firm that was associated in the trial conducted by IDRBT, is India’s diversity and challenges associated therewith. India has the fifth-highest number of billionaires in the world as well as the highest number of people below poverty line. “The idea is, if you are successful in India, you can virtually do it anywhere,” quips Chenard.

India is also the world’s top remittance receiving country. According to the Migration and Remittance Factbook published by the World Bank, India received USD 72.2 billion worth of remittances in the year 2015, though that is estimated to come down a bit in 2016. According to the recently published Infosys research, global financial services organizations have identified cross-border payment as the top priority use case of blockchain. No country will gain as much from a more efficient execution of cross-border payments as India will.

India’s large unbanked population and the recent government thrust to bring them to the financial system is another factor that would force financial institutions and the central bank to look at any efficiency enhancing technology that can effectively address the challenge. Blockchain, which is being tested for digital identity management purpose by many banks around the globe can be a potential winner.

And finally, there is the overall thrust on digital in general and digital payments in particular by the current regime in Delhi. The prime minister’s thrust on digital governance and efficiency will surely be a catalyst for most disruptive technologies that are secure and reliable.

Industry/market-related factors

Traditionally, financial services has been India’s strength. In World Economic Forum’s Global Competitiveness Ranking, that is the area where India always scores better, often ranking ahead of many developed economies. New private Indian banks have been known to be early movers when it comes to leveraging technology in general and Internet in particular.

The balanced approach followed by Indian central bank, Reserve Bank of India, is another major factor in any new technology adoption in Indian banking sector. In the last few years—especially during the governorship of Raghuram Rajan and his successor Urjit Patel—RBI has taken a cautious but pragmatic view of embracing new technologies, often forcing technology adoption on banks through regulation, wherever it has seen scope to enhance customer experience and efficiency using a particular technology. RBI’s proactive push of new technology adoption has not just been restricted to creating policy frameworks. It has used a mix of regulation, evangelism and even worked with the industry to make things easier and effective. The creation of National Payment Corporation of India (NPCI) which has significantly brought down the cost of electronic transactions is a case in point. The regulator also has an academic/research unit, Institute of Development and Research in Banking Technology (IDRBT) which keeps studying the opportunities and challenges in new technology areas. It is not a coincidence that both these units have been actively involved in testing out blockchain as a proof of concept.

However, despite all the proactive stance of the regulator and a few banks, Indian banking sector has not been able to cut cost of banking services drastically. This is something that made former governor Raghuram Rajan to openly express his disappointment. Speaking in an IDRBT conference in late 2014, Rajan said the cost structure in the banking system was still “significantly high” despite use of all the information technology.

“We can see the effect of the IT revolution everywhere in the banking system, except on the expenses side,” he said. “Why aren’t the expenses coming down?” he asked. “It is only by reducing the cost of transactions (that) we can reach all,” he said. This came after his criticism of the hasty rollout of Prime Ministser’s Jan Dhan Yojana. Virtually, he was challenging short term government push without having a long-term plan to make the initiative sustainable.

And he had a point. All that banks have done is to do the things the old way, but a little more efficiently and with more convenience to the customer but have not rediscovered the model itself to leverage the new technology era.

Blockchain comes as a perfect godsend to achieve this objective.

Tech/supply side ecosystem

The third important aspect—and India’s position is quite unique here—is the fact that India is a tech-hub. Apart from being a large technology outsourcing destination, India is also the home to vendors with large core banking market share globally. Two of the top three core banking solution vendors—Infosys and TCS—are headquartered in India .

Of late, India has also seen a lot of activity in the fintech arena. The country has become one of the global fintech hubs. While in many developed markets fintechs and banks have enjoyed an uneasy relationship, in India, most progressive banks like ICICI Bank, Axis Bank and HDFC Bank have proactively gone to fintechs, creating contests and hackathons to get the best of innovations, sometimes even sharing their APIs with these fintechs.

In short, India is today a vibrant powerhouse of fintech. That will—and the early signs only confirm the trend—impact blockchain trials, rollout and deployment in a unique manner in India, making it a global learning testbed.

Balanced approach, did you say?

RBI, which has been praised for its balanced approached, started with a customary note of caution.

In a press statement dated 24 December, 2013 RBI cautioned against the use of virtual currencies ‘including Bitcoins’. “The creation, trading or usage of VCs including Bitcoins, as a medium for payment are not authorised by any central bank or monetary authority. No regulatory approvals, registration or authorisation is stated to have been obtained by the entities concerned for carrying on such activities,” the statement said.

However it also clarified that RBI was “examining the issues associated with the usage, holding and trading of VCs under the extant legal and regulatory framework of the country, including Foreign exchange and payment systems laws and regulations.”

Exactly two years after that, in December 2015, RBI’s Financial Stability Report went all out for blockchain. Devoting a full section to blockchain titled Implications of disruptions –Blockchain technologY, it said, “Regulators and authorities need to keep pace with developments as many of the world’s largest banks are said to be supporting a joint effort for setting up of ‘private blockchain’ and building an industry-wide platform for standardizing the use of the technology, which has the potential to transform the functioning of the back offices of banks, increase the speed and cost efficiency in payment systems and trade finance.”

The intent was quite evident. In less than a year, Indian banking industry was ready with some trials. RBI, continuing its proactive stance, asked its academic and research unit, IDRBT to work on the area. And soon, the institute had taken multiple steps. While it was getting ready to do a field trial, it had studied the technology and its broader applicability to Indian banking system. It has also formed a Blockchain Working Group, with representatives drawn from RBI, commercial banks and tech companies.

“We will be holding a few workshops bringing bankers and solution providers together to have further deliberations on the points and pointers indicated in the whitepaper (on blockchain),” says Dr AS Ramasatri, director of IDRBT.

PoCketing Learning

With stakes high and with a supportive regulatory regime and technology ecosystem, it is natural that Indian companies have decided to take a dive. Half a dozen organizations have successfully completed proofs-of-concept, many more have initiated the efforts.

In the last six months—and that is when the action started—most of the new private sector banks have initiated blockchain PoCs.

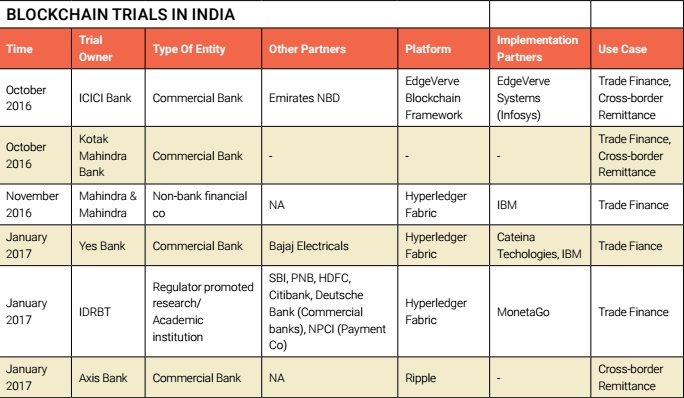

In October 2016, ICICI Bank announces successful completion of pilot transactions via its blockchain network with Emirates NBD on a custom-made blockchain application, co-created with EdgeVerve Systems, a wholly owned subsidiary of Infosys. One transaction was executed to showcase confirmation of import of shredded steel melting scrap by a Mumbai-based export-import firm from a Dubai-based supplier. The other one on the blockchain application was a transaction that enabled an ICICI Bank branch in Mumbai to remit funds to an Emirates NBD branch in Dubai in real time.

January this year saw a series of announcements of successful completion of PoCs by a few banks.

Yes Bank announced implementation a vendor financing solution which allowed its anchor client Bajaj Electricals to digitize the process for discounting and disbursal of funds to its vendors by integrating seamlessly with the bank’s systems. The blockchain-based smart contract has been written by fintech start-up Cateina Technologies and leverages IBM Watson Conversation, a cloud-based cognitive service and is built on Hyperledger Fabric supported by IBM.

Axis Bank, India’s third largest private sector bank, also announced a trial using an alternate blockchain technology, Ripple. It is testing the PoC to try out cross border payments.

Though not officially announced, according to media reports, Kotak Mahindra Bank too initiated a blockchain pilot, for transactions in cross-border remittances and trade settlements.

That means there’s news from all four of the top private banks in India about blockchain trials.

But there’s a non-banking company too. And it is an interesting case. In November 2016, IBM and Mahindra & Mahindra announced development of a blockchain. The pilot, to enable supplier-to-manufacturer trade finance transactions through a permissioned distributed ledger, was completed in December 2016. The blockchain for Mahindra & Mahindra is designed to transform supplier to manufacturer trade finance transactions. According to Jaspreet Bindra, Sr Vice President, Digital Transformation, Mahindra & Mahindra, who spearheaded the pilot in the company, the current invoice discounting application of blockchain in group company Mahindra Finance is just a beginning. “We will see where else can it create an impact within the entire group,” Bindra says explaining why a non-banking company like Mahindra went all out for the trial. He says production deployment can happen anytime now and does not rule out the possibility of making it available as a solution to others.

Apart from commercial organizations, IDRBT, the research unit of Indian central bank, RBI, too has conducted a successful, using the Hyperledger Fabric platform. New York-based fintech firm MonetaGo was involved in implementing it. While NPCI provided the payment inputs, five banks were involved for providing inputs on business processes and test scenarios and were involved in the review. The trial involved domestic trade finance letter of credit as a use case. Like all such trials, the thrust was on testing that it actually works and with transparency. IDRBT published the results in a whitepaper released in February.

Early Trends

It is just the beginning. Yet, early signs do indicate some definite—and perhaps logical—trends.

The most important and most visible is the use cases that Indian organizations have gone for. While most of the central banks, including Bank of Canada, People’s Bank of China and Monetary Authority of Singapore have gone for testing digital currency applications, Indian central bank has chosen to take a cautious approach and go for use cases “where it benefits most with least disturbance to the existing systems”. The famous ‘balanced approach’ of RBI is clearly visible here too.

In the Infosys research released recently, globally banks have identified cross-border payments, digital identity management, clearing & settlement, invoice financing and letter of credit process, in that order, as the priority. India has seen test cases for all, other than digital identity management. That is because with a system like Aadhar in place, the low-hanging fruits in digital identity management do not require an untested technology like blockchain. Aadhar itself can handle that.

While clearing and settlement and smart contracts may take a while, peer to peer payments is not going to happen anytime soon, till people at large and the regulator are convinced about security.

In terms of technology, Hyperledger Fabric clearly seem to be leading, though Ripple has made an inroad.

What’s Next?

Needless to say newer use cases will be tried. “In the inter-bank segment, centralized KYC can be of great benefit. Similarly, syndication of loans can be a potential area of application,” says Dr AS Ramasastri, director IDRBT.

As organizations move from trials to productions, there are indications that serious investment is being planned in trade finance and cross-border payments. But it is a question of first few days. Once the system gets tested and internalized, the growth will be far more rapid.

Blockchain is a technology which, by definition, works on the principle of sharing—sharing the ledger. It requires interbank collaboration to really move forward. With regulation still restricted to national boundaries, it is difficult to expect that operational collaborations involving banks in different geographies will become a reality soon, except where it is a basic need, such as cross-border payments.

Many countries such as Australia, China, Canada and Japan have formed regional consortia of banks. Reportedly, India may see such a consortium soon. State Bank of India, India’s largest bank, has reportedly started a consortium of banks and other organizations to create a multi-party permissioned blockchain, called Bankchain. It is reported that 10 commercial banks such as ICICI Bank, Axis Bank, Central Bank of India, DCB, Deutsche Bank, HDFC Bank, IDBI Bank, Kotak Mahindra Bank and Saraswat Bank are likely to be part of the consortium that include IBM, Microsoft, KPMG and Skylark.

What India may well lead in—Mahindra & Mahindra’s case is just one example—is the application of blockchain into non-banking areas such as public services. Land records and the planned property database are ideal testbeds for a shared ledger. If done successfully, they could pave the way for many such applications around the world.

While opportunities are immense, there are challenges that remain. These challenges could be operational, technological as well as regulatory. Initially, they will be operational as no commercial company will get into something while testing out a new technology where current regulation may not be adequate/relevant.

Infosys research among global banks identified six key challenges, with top three being readiness of ecosystem and need for cooperation within banks, integration of blockchain applications with existing enterprise applications, lack of governance model among stakehokders.

In India, cooperation among banks may not be too much of a challenge because RBI usually takes a proactive step to bring them together and does not shy away from making its hands dirty, if required, as it has done in payment systems by actively promoting NPCI. IDRBT has been mandated to do that for blockchain.

Another possible regulatory change could be how transactions get reported to the RBI. In a consortium-based permissioned blockchain, significant governance function will remain with the consortium and not the individual banks. Since the transaction will be recorded on the distributed ledger, logically, it is the consortium that should report to the regulator. That requires significant changes to regulation.

Today, consortiums do not even have their own governance models. Global lessons will be important.

Once a distributed ledger is implemented, the question arises is if the regulator will have access to the transaction level information. Some experts, including Rajashekhara V Maiya of EdgeVerve say, the regulator may possibly have access to read but not modify. Nevertheless, for the user, it could be a privacy issue that needs to be tackled by the bank.

How the current technology investment of banks gets protected may also emerge as a technology challenge. Whether blockchain can work with the existing core banking, what changes will be required will be important questions. But we expect that banks will first leverage blockchain in areas that are fairly isolated from traditional consumer and corporate banking and are fairly isolated from those processes. They may well satisfy the criteria of Dr Ramasastri, “where it benefits most with least disturbance to the existing systems.”

So, by the time they are confident with blockchain as a technology, some of the questions on technology integration would probably have been adequately addressed.

Lest we forget, the current enthusiasm and feel-good is based on success of PoCs. But as Dr Ramasatri clarifies, “A proof of concept is some kind of demonstration and not full scale deployment. It has its limitations.”

None of the non-functional requirements have been tested in the PoC as the objective was to test that the technology works and can deliver the functional requirement without any hiccups. In fact, very recently, RBI deputy governor R Gandhi warned that the potential of blockchain may be overstated, though he was speaking mostly in the context of virtual currencies.

But there is no denying that there are certain applications/use cases that can be moved to blokchain right away without much disturbance to the rest of the business and with significant efficiency gains.

Initially, most of the use cases are looking for efficiency gains but once the system matures and if blockchain actually delivers on its promise of being a more trusted platform, business organizations will be able to bring down the risk considerably.

That will help them try newer things. Says Sriram Raghavan of IBM, “The next level of innovations will really come with new products, because you have taken away risk too.”

It may create completely new business models. As with any new technology, it is always applied to enhance the existing processes before people begin to realize that they can do things completely differently, or part of the process becomes redundant in the new scenario and so on. Blockchain will obviously see all of that, so fundamental is its impact.

And we do not need to wait for long to see how it shapes up. Going by the prediction of Maiya of EdgeVerve, all those banks that have done their PoCs will go for production in next six to eight months. That is this year.

So, 2017 may well become the year of the blockchain.